Newsletter commentary Dec 2021

Time:2022-01-01

Time:2022-01-01

2021 has passed. The environment has had a significant impact on investment, which we discussed a lot in the recent investor meetings and in articles posted on our public account. In this commentary, we would like to have a review on the market in 2021 as well as an outlook on our focuses in 2022.

In 2021, CNI 2000 rose by 29%, ChiNext rose 12%, CSI 500 rose 16%; CSI 300 fell by 5%, SSE 50 fell 10% and China Concept Stocks fell around 50%.

From an industry perspective, Consumer Services fell by 24%. The Service industry was seriously hit by the pandemic, and the Education by policy. The Duty-free Concept stocks suffered from a high valuation in the beginning of 2021, hence the high growth in the performance still unable to withstand the decline in valuation throughout the year. Non-bank Financials fell by 20% mainly drugged by Insurance, towards which the market has had a new view. The performance of Brokers was not bad, but the valuation in the beginning of 2021 was high. The business model of the brokerage firms has been improving with a larger market, wider-ranged services, and a better competition in comprehensive capabilities rather than a homogenized one. The Property sector fell by 10% and the Home Appliances by 19% with the market expectation of an already peak in real estate and with the future uncertainty. The Food and Beverage fell by 5%, because the original long-term stable growth was speculated into high growth and high valuation during the pandemic, and then the growth was found unsustainable, hence a return in valuation. The Pharmaceuticals fell by 4%. Stocks benefited from the epidemic has fallen. The enlarged centralized procurement has hit the logic of pharma stocks. CXO has been the highlight of the year 2021, which was sought after in the end of the year with the supportive policies on Chinese medicine. In the long run, they will also be subject to Pharmacoeconomics. The consensus for pharmaceuticals looks for the overseas market and real innovation. New energy for power equipment is the winner of 2021 that rose by 50%. The annual photovoltaic installation was lower than expected due to high price, but the shortage of silicon materials and chips has boosted some links in the chain to gain profit beyond expectation. The year 2021 was a booming year for offshore wind power too. The overall valuation of power equipment rose sharply. New Energy Vehicles have exceeded expectations all the way with sales rising by more than 150% YOY and monthly penetration rate reaching 20% in the end of 2021. Power Equipment is an industry with ordinary business model but high growth. In 2022, the market expects that a cost reduction of RMB0.3 per watt, brought about by the no longer in shortage silicon materials, will boost the installation as well as the profit in the non-silicon links of Photovoltaic industry. This looks possible from a quarterly point of view but not necessarily from annual, as the profit will eventually be transferred to the downstream operators who will only see short-time profit and will very probably be required to improve the quality of power supply that will increase their cost. The challenge of New Energy Vehicles comes from rising costs, but except for Tesla, not any other players would raise prices due to fierce competition. Meanwhile, chips will no longer be in shortage in 2022. The prices of traditional vehicles may need to be reduced facing pressure from the new energy competitors. It is uncertain whether the focus of the market will shift if the penetration of the latter exceeds 20% without making profit. Chemicals rose by 48% in 2021 because a) the anchor of valuation has changed against energy consumption control and new demands created by new energy; and b) expansion plans. Non-ferrous Metals rose 46% driven by energy consumption control and by the demand of new energy that caused price increases of several metal products. These products were in high demand but the production expansions were relatively slow. Coal and Steel also increased by more than 40%. The former was because of demand beyond expectation. After the increase in approved production, supply and demand of coal was in a tight balance. The tilt of the balance will depend on the amount of imported coal, the new capacity of production and the change in power demand in 2022. The latter was because of production restriction. The future of Steel will depend on the balance between production restriction and real estate development.

There might be some changes in 2022. First, the share of manufacturing in the economic structure has been largely lifted by exports, but the growth of exports in the past two years was abnormal under the pandemic. For many years before the pandemic, China’s exports had been basically in line with economic growth, and its share in global trade had been stable. However, for the past two years, such share has risen from 13% to 17%, marking a sudden and significant macro variation that brought major impact on many occasions. Such as energy demand – China’s energy consumption recorded a decent decline before the pandemic, but has been facing a big challenge after it due to the decrease in the proportion of the Service industry in the economic structure. In 2022, the ease of the epidemic and the situation of exports will have a significant impact on energy consumption and the other aspects. Second is inflation, which has been low in China and high overseas. The theory of a temporary overseas inflation is no longer valid. Inflation trends are disturbed by too many factors, such as liquidity, supply chain, labor participation, and energy prices. In general, inflation will support interest rate increase, therefore the impact of tightening overseas liquidity needs to be paid attention to. Third, although the goals of carbon peaking and carbon neutrality won’t change, the path may shift from a campaign style to an optimized combination that is more country-specific. Fourth is the strength of domestic policies focusing on economic development. Finally, the pandemic. Everyone is tired after the two years. The impact of the epidemic on each country has been different. As the situation changes, the advantages and disadvantages will change. The curb of the pandemic will be a major drive for the recovery of the Service industry and consumption.

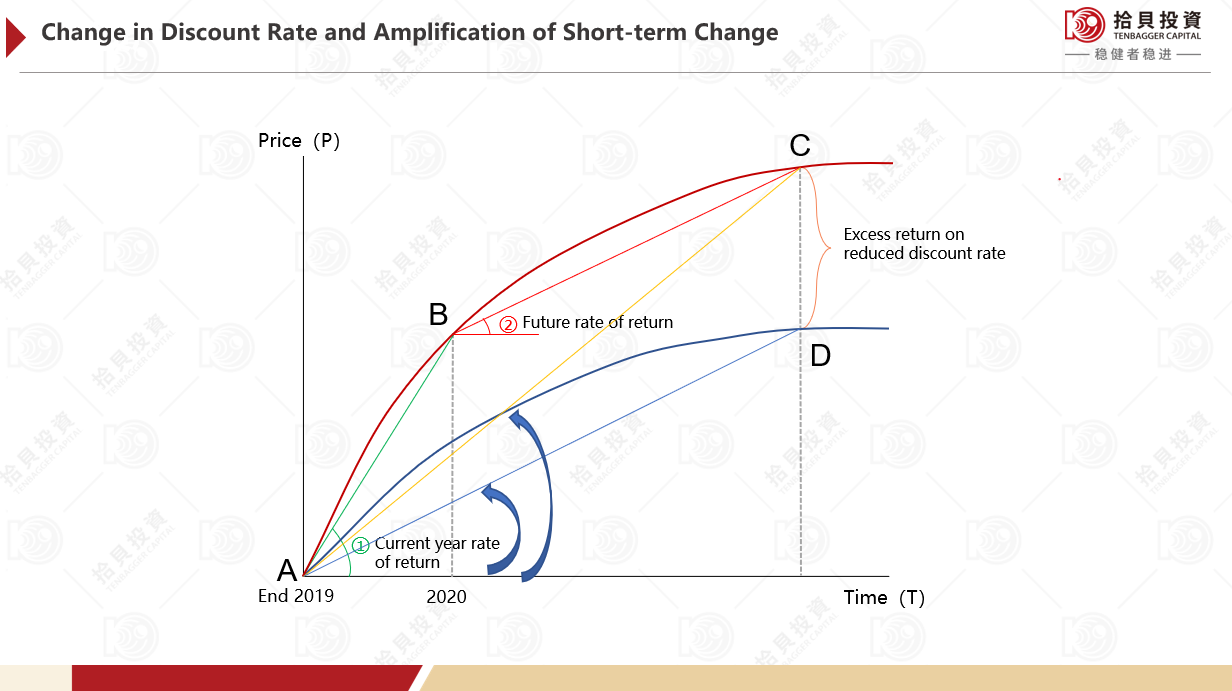

At the beginning of 2021, we tried to explain the changes in the market over the past period of time and the choice of future investment strategies with the above chart. To estimate the value of a company, its originally implied value curve was AD, and the embedded return was the slope of AD. In the past few years, whether because of advanced concepts, of the opportunity cost decrease when investing in stocks, of the entry into the market of investors expecting lower returns, or probably of ambitious assumptions by prophets about the future of the molecules, the discount rate of marginal price makers has fallen. Thus, the company’s value curve shifted to AC, and the embedded rate of return became the slope of AC. Another thing to be noticed is that AC is not a straight line but convex to the upper left. Therefore, the short-term rate of return will be much higher than the slope of AC. In fact, this is based on the subsequent decline in the rate of return.

In practice, the reduction of the discount rate is real. For A-share market, a greater possibility of discount rate decrease is expected than that of an increase in 2022, while the expectation for the overseas markets is the opposite. Meanwhile, the ups and downs of many industries in 2021 showed that the people’s accuracy in forecasting the future was limited. It was more of the current emotions rather than long-term rational expectations. Therefore, people tended to gain short-term high returns first from point A to point B, and entered the point B to point C stage where the rate of return decreases. At the same time, short-term changes are still very sensitive, reflected by the negative or low returns during certain periods on many Food and Beverage and Pharmaceuticals names.

The general mode of investment in A-shares, or of any investment might be to find out an AD curve with relatively large slope, wait for the others to imagine it as an AC curve, gain profit from point A to B, and move on to another AD curve. Finding AD curves is a basic skill and an anchor. Having them turned into AC curves is a luck. It doesn’t matter if the latter doesn’t happen. It’s already good to get return following the AD curve.

At the beginning of 2022, we don’t see any industry with particularly high return potential in the medium-term, nor do we see particularly big risks. The overall valuation of the current market is not expensive and the market is of a great variety. There might be changes due to multiple variables, and we will strive to make progress while maintaining stability. The future development of real estate industry is a risk, which we look forward to a smooth landing. The population issue can also be eased. The liquidity of the U.S. dollar will be tightened, while that of RMB will be loosened. We hope the pandemic to fade. Will all these be happening? If the pandemic situation turns positive, it will be a big plus to help solve many short-term issues. And this is possible. Finally, we wish you all a happy new year and a good luck in investment.